Quarterly Update

Nathan Geraci is President of The ETF Store, Inc. and host of the weekly radio show “The ETF Store Show“.

In many respects, the second quarter of 2016 was a case of “same song, different dance”, bearing striking similarities to the first quarter. You may recall the visual we provided in our last quarterly update, depicting the V-shaped stock market action during the first three months of the year:

Source: Bespoke

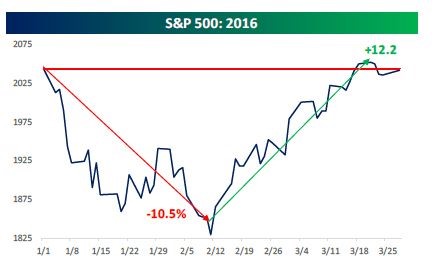

While not quite as dramatic, the market action during the last week of the second quarter looked awfully familiar:

Source: Bespoke

In the first quarter, an unpleasant mix of concerns over China’s economy, looming Fed rate hikes, the falling price of oil, and a corporate earnings recession conspired to drive down stocks before fears were soon allayed and the market recovered. In the second quarter, the United Kingdom’s vote to leave the European Union (the so-called “Brexit”) unleashed another wave of fear – only this time, the fear was even shorter-lived.

While there are certainly legitimate longer-term concerns over the U.K.’s decision to leave The Union, including whether there may be a cascading effect of other European countries holding their own referendums on leaving the E.U. and potential negative economic consequences, the Brexit’s impact on the market – at least for now – looks a lot like the other events that were short-lived. Examples would be the “Grexit”, the 2011 U.S. debt ceiling debacle, the Ebola virus scare, and most recently, the first quarter of 2016…much ado about nothing. However, as we enter the third quarter, a prudent investor may well be wondering what might finally bring an end to the 7+ year-old bull market – which brings us to the world’s central banks.

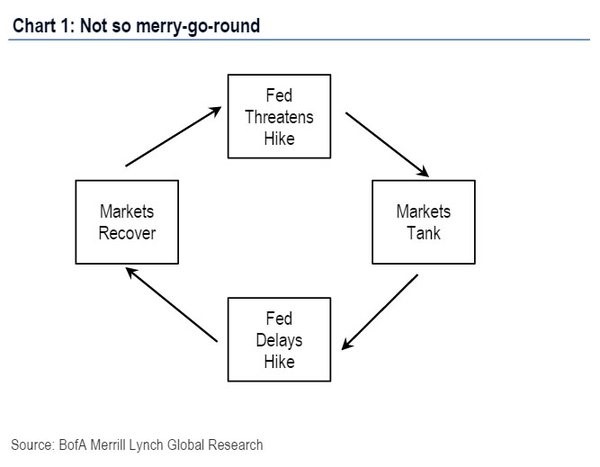

Central Bank Merry-Go-Round

After the 2007-2008 financial crisis, central banks around the world embarked on unprecedented stimulus in an effort to spark the global economy. This stimulus has resulted in varying degrees of success, but one thing is certain: as it relates to the financial markets, central bank stimulus has led us into uncharted waters, creating market distortions and leaving market participants unsure how to respond to both ordinary and extraordinary events. Whether it be the mix of issues we saw in the first quarter, the Brexit in the second quarter, or the always looming threat of Fed rate hikes, the markets initially react negatively to the news and then seem to quickly brush aside any concerns. To further illustrate this point, as it relates to Fed rate hikes, the following chart offers a crude, though accurate, depiction of the Fed “merry-go-round”:

Markets are now taking their cue from central banks, who appear to be taking their cue from the financial markets. Around and around we go. You could add events like “Brexit” to the above circular reference: the UK votes to leave the EU, markets tank, central banks delay hikes/offer more stimulus, markets recover, central banks threaten hikes/remove stimulus, and the next market event occurs. Central banks have helped create a market environment where the 10-year U.S. Treasury yield currently stands near all-time record lows, while U.S. stocks are at all-time record highs and offer a greater dividend yield than Treasuries. Are central banks supporting the global economy, supporting the financial markets, or both? What will the outcome be?

Mohamed El-Erian, of PIMCO fame and currently chief economic adviser at Allianz, summed-up the situation perfectly:

“Think of central banks like a doctor. They’re walking by, they see their patient—the global economy—in trouble. They will not walk away from the patient. They are wired to respond even if they don’t have the right medication. What happens when you respond for a very long time with the wrong medication? You start worrying about side effects, you start worrying about unintended consequences. That is where we are today.”

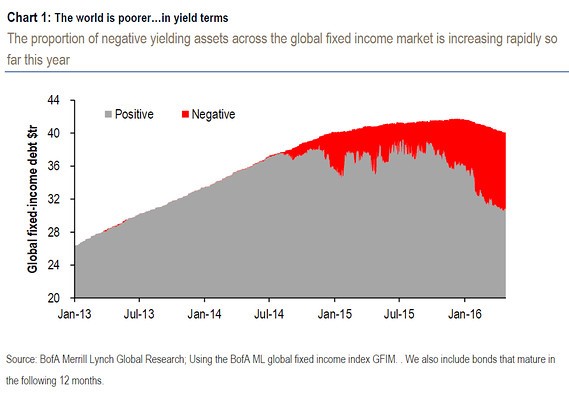

To further illustrate the point of central banks providing the wrong medication, consider the following two disturbing charts:

The first chart shows the increasing proportion of negative-yielding bonds across the globe, which is largely a result of central bank bond buying. What are negative yielding bonds? You willfully lend your money to, say, the Japanese Government, knowing in advance you will get less back than initially lent! Believe it or not, there are now roughly $10 trillion of these bonds around the world! And speaking of Japan, their central bank happens to be a top 10 shareholder in some 90% of their “blue-chip” stocks (second chart). The Bank of Japan is creating money out of thin air and using that money to purchase Japanese stocks. We could go on with similarly unbelievable charts, but you get the idea. There is nothing normal about $10 trillion in negative yielding bonds or a major central bank owning a huge chunk of a country’s major stocks.

So What Does This Mean for You as an Investor?

The best way to address the intended AND unintended consequences of questionable central bank policies is to have a plan in place now; NOT to scramble after the markets gap up or down based on headlines. As it relates to unintended consequences, they can best be thought of as risk. Risk comes from uncertainty. The actions of central banks around the world have created a tremendous amount of uncertainty in the markets. For investors, uncertainty can be both good and bad – there is upside risk and downside risk. That is the dilemma facing investors right now. Unintended consequences can lead to unexpected benefits or nasty surprises. As an investor, you must be prepared for both. Whether you have a limited investment horizon, or decades to reach the promised land, we are here to help guide you through these uncharted waters with a confident and intelligent investment plan.