Unpleasant Surprise: Mutual Fund Capital Gain Distributions

Nathan Geraci is President of The ETF Store, Inc. and host of the weekly radio show “The ETF Store Show“.

As the calendar turns to November and the end of the year quickly approaches, it’s time to start thinking about the tax consequences of investments you hold in taxable accounts. Taxes sometimes get lost in the shuffle when evaluating investments, but they can take a big bite out of returns. For investors holding mutual funds, particularly actively managed funds, you may soon receive an unpleasant surprise in the mail – notification of capital gain distributions. If you’re not familiar with capital gain distributions, quite simply, they are the payment (to you) of any net gains made from positions (stocks, for example) a mutual fund manager has sold during the course of the year. The fiscal year for most mutual funds ends on October 31st, so funds will begin announcing capital gain distributions soon and investors typically receive them in December. So why would payments made to you be unpleasant? You owe taxes on these payments if the mutual funds are held in a taxable account (in 2013, the top capital gains tax rate increased to 20%, with high income earners paying an additional 3.8%).

Consider the following basic example: Let’s say you own shares of a mutual fund and there is another shareholder in the same fund that wishes to sell their shares because they need cash to buy a house. In order to meet this redemption request, the manager of the mutual fund may need to sell shares of stocks held by the fund to raise cash necessary to pay this shareholder. When the mutual fund manager sells shares of stocks owned by the fund for a gain, the mutual fund is required by law to distribute those gains to all mutual fund shareholders – including you! And remember, those gains are taxable if you hold the mutual fund shares in a taxable account.

So to recap, if you’re a shareholder of a mutual fund and another shareholder redeems their mutual fund shares to buy a house, you may be penalized with a taxable capital gain distribution even though you didn’t do anything. That hardly seems fair. And what’s worse, these capital gain distributions are “phantom gains” in that the share price of a mutual fund is reduced by the amount of the capital gain distribution. So net-net, you haven’t gained anything other than a tax bill. According to the Investment Company Institute, in 2012, mutual funds distributed $99 billion in capital gains to shareholders.

Now, compare that with exchange traded funds (ETFs). If an ETF shareholder needs cash to purchase a house, they simply sell their shares through their broker or brokerage account with no impact to you. In other words, there’s no need for an ETF manager (provider) to sell shares of stock held by the ETF to raise cash. The ETF structure itself also lends to greater tax efficiency. When ETF shares are created and redeemed, the underlying securities are delivered “in-kind”. This means shares of the underlying stocks are exchanged for shares of the ETF (and vice versa) – there’s no taxable event. A benefit of this process is that ETF providers can shed their lowest cost basis shares of stocks (which have the largest capital gains). There are instances where ETFs may reconstitute or rebalance holdings, thus generating a capital gain distribution, but those instances are rare. The bottom line is that with ETFs, you have significantly more control over when you realize taxes, as opposed to with mutual funds, where you’re at the mercy of other shareholders.

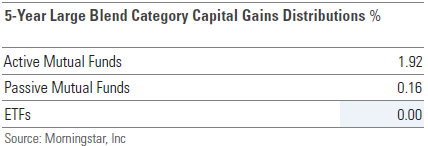

In addition to ETFs providing you with more control over when you realize taxes, it’s important to point out that another, more significant component of ETF tax efficiency is that most ETFs are passively managed. In other words, they simply track an index instead of paying a high priced manager to attempt to pick individual stocks for the fund (which, historically, they haven’t been very good at – but that’s a discussion for another time). This means lower turnover (less buying and selling) of the underlying stocks in the fund. And that means fewer taxable events. The below chart from Morningstar’s “ETFs Under the Microscope: Tax Efficiency Survey” shows how capital gain distributions for actively managed mutual funds, passively managed mutual funds, and ETFs compare in the large blend category:

Also, consider that in 2012, iShares – by far the largest ETF provider, did not pay capital gain distributions on 98% of their 280 ETFs.

So, what can you do to protect more of your hard earned money from Uncle Sam? If you must buy a mutual fund, wait until after the fund pays out its capital gain distribution before you buy. You can generally check with the mutual fund provider website to find that date. If you already own a fund and it hasn’t yet paid its capital gains distribution, you can avoid the distribution and still retain much of the performance of the fund by selling the fund and buying a highly correlated ETF that tracks the same or a similar benchmark. You can use ETF Database’s mutual fund to ETF converter tool here to help you in that process. Finally, as the calendar turns to a new year, you might consider making ETFs a bigger part of your portfolio to minimize these headaches altogether.

Fidelity (Finally) Makes Jump into ETFs

While ETF assets have surged over the past five years, nearly tripling, Fidelity has watched assets in their actively managed stock mutual funds shrink 16% and corporate profits shrivel up. We hate to say “we told you so”, but back in 2009, we explained why Fidelity had better move quickly to avoid “getting their lunch eaten by the ETF competition”. Even then, it was clear that investors were quickly gravitating to low cost, tax efficient, and transparent ETFs. Furthermore, investors were becoming acutely aware of the underperformance of active mutual fund managers, which is where Fidelity butters its bread. At the time, Fidelity was concerned that lower cost ETFs might cannibalize their lucrative actively managed mutual fund business. Remember, actively managed mutual funds are typically significantly more expensive than ETFs – which means more of your money in the pockets of mutual fund companies instead of your investment accounts. Quite simply, Fidelity was content to watch what has been called “the next generation mutual fund” leave the train station without them.

Fast forward to today and, as they say, “better late than never”. After essentially standing on the sidelines for the better part of a decade, Fidelity is finally making their first real push into ETFs. They did launch a single ETF (ticker ONEQ) some ten years ago, but this was really a token entry into the ETF market with no real corporate ETF strategy in place. Today, Fidelity is making a concerted effort to play catch-up with the launch of 10, passively managed sector ETFs. What’s particularly interesting about this initial lineup of ETFs is that they’re undercutting similar sector ETFs from low cost leader Vanguard. In other words, Fidelity is not just quietly entering the ETF business – they’re going for the jugular. It’s also noteworthy that Fidelity already offers one of the largest lineups of sector mutual funds, including 44 that are actively managed. That means there’s a pretty good chance that Fidelity does, in fact, cannibalize its own business. The fact that they’re willing to do so makes a pretty strong statement about their belief in the future of ETFs.

So what are the takeaways for investors? 1) One of the world’s largest, most well-known mutual fund companies is making an aggressive push into ETFs. That should tell you something about where the future of the investment industry lies. We won’t go so far as to say mutual funds will become obsolete, as some prominent industry professionals have, but there’s no denying the massive trends in play here. 2) Investors are driving this change. They’re voting with their own money and they want low cost, passively managed products – not expensive, underperforming ones. Ultimately, companies have to listen to the consumer. In some regards, Fidelity is fortunate that they still have an opportunity to “catch the train” after basically ignoring obvious consumer trends. 3) If you’re not at least considering investing ETFs, it’s time to ask why. Mutual fund companies Vanguard, PIMCO, and now Fidelity are all aggressively involved in ETFs. Charles Schwab launched a full ETF platform. Times have changed and technology evolves, even in the investment business. While mutual funds may have been the past, ETFs appear to be the future. A future that Fidelity is now betting heavily on.

Commission-Free ETF Push Continues

Listen to The ETF Store Show every Tuesday at 9am on ESPN 1510 as we cover everything you need to know about Exchange Traded Funds and the world of investing.

Click here to listen to The ETF Store Show now.

Charles Schwab recently introduced 16 additional commission-free ETFs on their Schwab ETF OneSource platform, which now features a total of 121 commission-free ETFs. On our most recent radio broadcast, we explained the broader significance of this move and discussed where ETF commissions should factor into the decision-making process when evaluating ETFs for your own portfolio. We also looked at the telling results of a new ETF investor survey from Schwab which, among other things, found that half of the respondents plan to increase their ETF holdings over the next year – a 22 percent increase over those who said the same in 2012. Beth Flynn, vice president of Schwab’s ETF platform management, summed up the survey results, stating that “demand is up across the board, and investors who own ETFs appear to be more interested in the product than ever – we’re seeing less discussion of ‘if’ and more about ‘how’ investors will buy and use ETFs”. On the show, we explained why a growing number of investors are moving to ETFs and why you shouldn’t expect to see this trend slow down any time soon.

In our weekly market update, we provided the key details on the last minute deal reached in Washington to reopen the government and raise the debt limit. While politicians, once again, “kicked the can down the road”, continued dysfunction in Washington could ultimately become a real concern for the US economy and of course, the stock market. In our ETF spotlight segment, we highlighted the Vanguard Small Cap ETF (ticker VB). For longer-term investors, small cap stocks can offer the potential for growth and also some diversification benefits in your portfolio. Since 1926, small cap stocks have outperformed large cap stocks by about 2% a year. VB offers an extremely low cost, efficient way to access small cap stocks. Learn more about VB and other Vanguard ETFs by visiting etfbuzz.com.