Nate Geraci

October 11, 2018

Nathan Geraci is President of The ETF Store, Inc. and host of ETF Prime.

After limping to a 2.5% gain during the first six months of the year, the S&P 500 surged more than 7% in the third quarter to all-time highs. Stocks posted strong gains despite global trade concerns, rising interest rates, partisan political discourse, and a bull market some view as long in the tooth. Underpinning the market’s ascent was a healthy economic backdrop, with the latest measure of GDP showing a 4.2% annual growth rate and unemployment near 50-year lows. U.S. companies are riding the wave of an increasingly buoyant economy, aided by a tailwind of corporate tax cuts. According to FactSet, estimated third quarter earnings growth for S&P 500 companies is 19.3%, which would mark the third highest level since early 2011.

While the economy has undoubtedly been positive for U.S. stocks, it has been a double-edged sword for well-diversified investors. Economic strength has resulted in rising short and long-term interest rates, pressuring bonds (remember, bond prices move in the opposite direction of interest rates). Also, an improved domestic economy has translated into a stronger U.S. dollar. That, combined with tariffs and trade tensions, has created a challenging environment for international stocks. The end result is a less-than-satisfying scenario where U.S. stocks have performed well, but not much else.

As it relates to bonds, most investors understand they provide income and serve as a portfolio ballast, offering stability during periods of stock market turmoil. However, while it’s one thing for bonds to trail the stock market, it’s another thing entirely for bonds to lose money. Consider the bellwether bond market benchmark, the Bloomberg Barclays Aggregate Bond Index. This benchmark has only experienced three negative years since 1976. Through September, it’s down nearly 1.7%. While a 1.7% decline might be a bad day in the stock market, it’s not something bond investors are accustomed to.

Where rates go from here is anyone’s guess – though indications point to future increases, which could cause more short-term pain for investors. However, it’s important to remember the role bonds play in a portfolio. At some point, U.S. stocks will experience declines and bonds should help provide a buffer. Also, as rates rise, investors receive higher interest payments – a pay raise without doing anything. Over the long-term, those pay raises offset short-term principal losses.

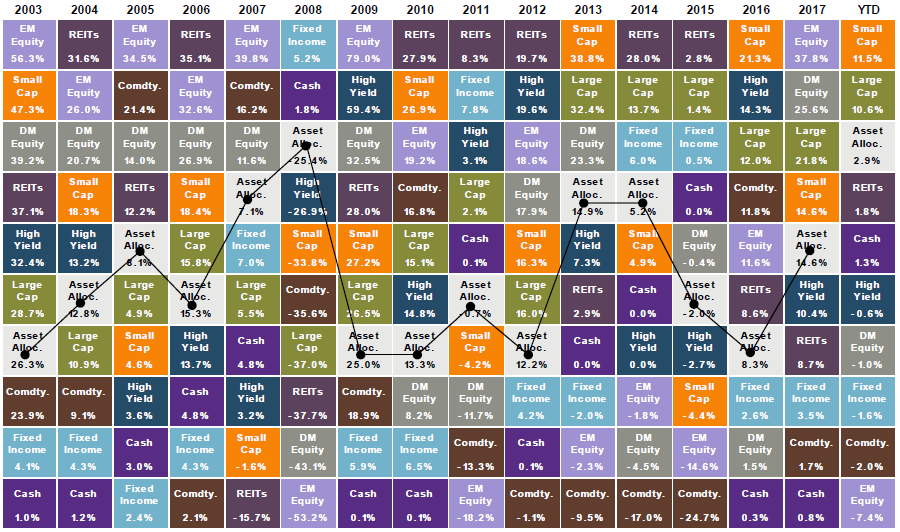

As it pertains to international stocks, there are several key points to keep in mind. The U.S. only represents about 55% of the world’s total stock market capitalization. In other words, if you don’t own international stocks, you are missing out on 45% of the world’s stocks. Those kicking themselves for owning international stocks this year only need to look back to 2017. Emerging market stocks were a top performing asset class at +37.8%. Developed international stocks were +25.6%. As a matter of fact, emerging market stocks have been one of the top two performing asset classes in 7 of the past 15 years.

The above chart is typically referred to as an “asset class quilt” – one randomly strewn together with no rhyme or reason. There should be two obvious takeaways from this colorful quilt: 1) U.S. stocks will not outperform every year, and 2) Attempting to predict which asset classes will outperform is a fool’s errand.

Over the long-term, owning a globally-diversified portfolio which includes bonds and international stocks can improve your overall risk-adjusted returns. Embrace diversification. While you will never own 100% of the best performing asset classes, you will never be overloaded on the worst. Notice the “Asset Alloc.” on the chart, connected by dots and lines. This reflects a well-diversified portfolio of U.S. stocks, international stocks, emerging markets, bonds, commodities, and REITs. This is what wins the race over the long-term.

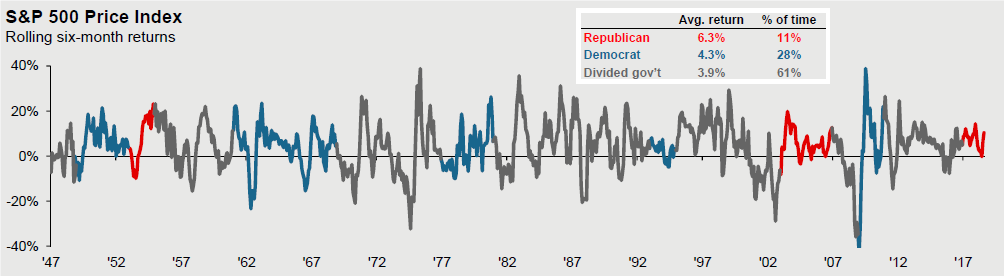

Lastly, speaking of races and fool’s errands, I’ll close with a comment on the upcoming congressional elections on November 6th. You will likely see a multitude of articles and charts proclaiming the market does this or does that following mid-term elections. Ignore them. While stocks may experience short-term volatility surrounding elections, for long-term investors, it simply doesn’t matter what the market does 3, 6, or even 12 months following mid-terms. Historically, there is no meaningful, long-term stock market pattern depending upon whether Republicans or Democrats are in control, or if we have a divided government. Even if there was a discernible pattern, the stock market doesn’t always go by script (see stocks’ reaction to the 2016 election). We also have an extremely limited data set given mid-term elections are only held every 4 years, which further calls any “patterns” into question.

That’s not to minimize the impact government can have on our lives and the broader economy. Depending upon the election outcomes, there may be all sorts of topics bandied about: investigations, impeachment, trade wars, tax reform, healthcare, infrastructure spending. Given today’s highly polarized political environment, some or all of these topics might evoke an emotional response. But as with most everything in investing, emotion is best checked at the door.

With Thanksgiving upon us this quarter, one of the golden rules of the family turkey dinner is to avoid the temptation to talk politics. Mixing politics and stuffing has a way of resulting in indigestion. It’s the same with politics and investing. Politics is short-term noise. There is a cornucopia of outcomes that could transpire longer-term, most of which will be difficult to predict. What we can all agree on is we have the fortune of living in the greatest country on earth. The political landscape will have its ebbs and flows, but the country always moves forward and progresses over the long-run – just like your investments.