What Goes Up Doesn’t (Necessarily) Have to Come Down

Nathan Geraci is President of The ETF Store, Inc. and host of the weekly radio show “The ETF Store Show“.

The 2017 stock market might best be characterized as long in frightening headlines, short in volatility, and strong in returns. The S&P 500 registered its second-best year since 2009, despite a seemingly never-ending flow of negative news. The Robert Mueller investigation, growing tensions with North Korea, devastating hurricanes, overseas terrorist attacks, horrific domestic shootings, Charlottesville – the headlines were enough to give even hardened investors pause.

Remarkably, despite it all, the S&P 500 closed every single month of 2017 with positive gains – the first time that has ever happened. That monthly winning streak actually extends back to November 2016 and stocks have now increased in 21 out of the last 22 months! Volatility has been virtually non-existent. The S&P 500 went the entire year without an intraday decline of more than 3%. The largest gain? 1.4%. Stocks essentially “melted up” in the lowest volatility year on record. Notably, foreign stocks fared even better in 2017, with developed international stocks gaining nearly 27% and emerging market stocks jumping over 31%.

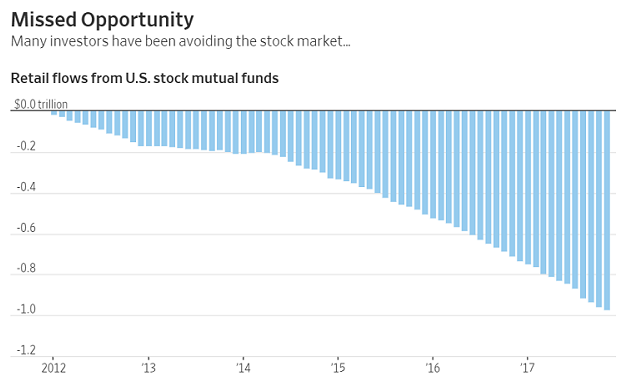

In last quarter’s commentary, we discussed how to survive a bull market. As stocks continue rising, like the S&P 500 has done every year since 2009, investors have a natural inclination to become more risk averse. There is a growing urge to take some winnings off the table. The following chart illustrates this, with investors increasingly pulling money out of mutual funds as stocks continue their ascent:

Source: The Wall Street Journal

Now, it should be noted that an estimated 40% of these outflows consist of money being pulled from expensive, underperforming active mutual funds and being invested into lower cost ETFs. Also, some investors may simply be rebalancing or repositioning into other areas such as international stocks or fixed income (though that still points to a desire to reduce exposure to U.S. stocks). Nonetheless, a meaningful portion of outflows can be attributed to some investors growing ever more cautious. The prevailing narrative among these investors is that stocks cannot continue to post gains year-after-year and valuations are overextended. However, by taking money off the table, these investors miss out on subsequent returns as the bull market continues charging ahead. That is why bull markets can be so difficult for investors to “survive”.

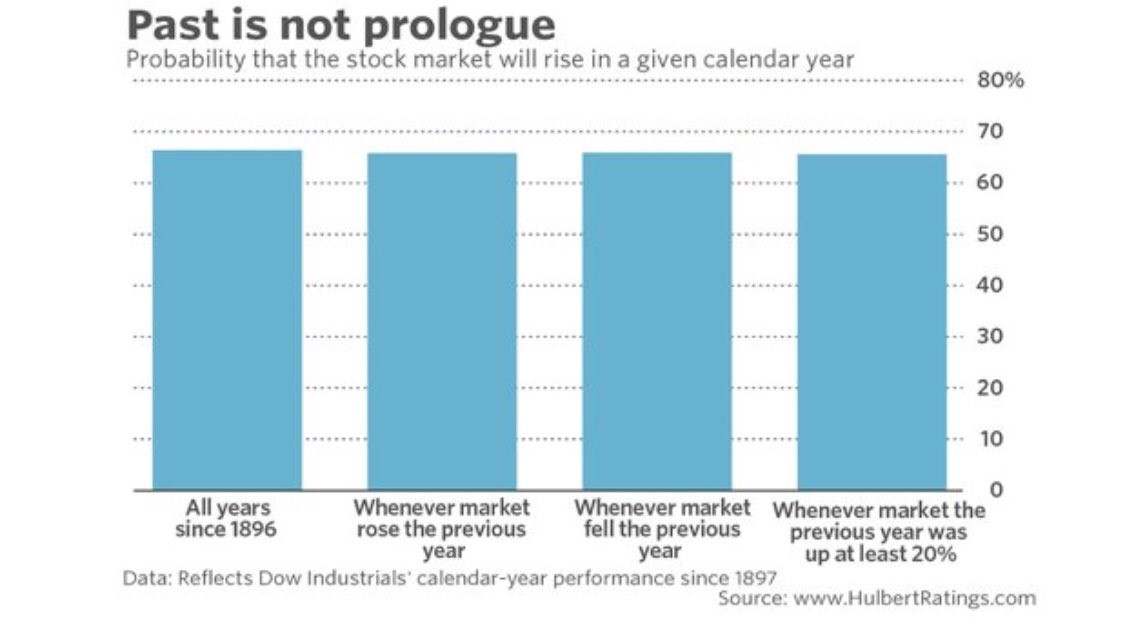

As it relates to stock valuations, it is important to remember they tend to be poor market timing tools. While stocks are on the pricey side, they can remain so for long periods of time. Valuations are meaningful indicators of the probability of future returns (i.e. when valuations are high, future returns are likely to be lower – though not necessarily negative), but their ability to predict shorter-term market moves is extremely limited. In terms of the stock market’s ability to post gains year-after-year, consider that according to The Wall Street Journal’s Market Data Group, when the S&P 500 has gained at least 19% in a particular year as it did in 2017, it has managed to produce a positive return the following year 68% of the time (with an average gain of 8%). In other words, just because the market has gone up, that does not indicate a higher likelihood of a decline. The probability that stocks will rise is actually consistent across a variety of scenarios going back to 1897 (using the Dow Industrials):

Source: The Fat Pitch

That is not to say the market cannot or will not decline in 2018. The fact that stocks have increased for 14 straight months without an intraday decline of even 3% is highly unusual. It is not realistic to expect that to continue. A normal year in the markets typically includes a roughly 10% decline in stocks at some point. According to JP Morgan, since 1980, the average intra-year drop has been 13.8% (though note that annual returns have been positive in 29 of those 38 years). Volatility is a normal part of investing in stocks and, as an investor, you should be mentally and financially prepared for it. The Robert Mueller investigation is still ongoing. The saber-rattling between the U.S. and North Korea has only intensified. Mid-term elections are on the horizon, which could shift the balance of power and the political landscape. There are always “unknown unknowns”.

On the other hand, the U.S. economy and corporate earnings continue to grow. The U.S. economy is currently experiencing its third-longest expansion in history and may reach its second-longest by midyear. The new tax bill, along with a possible infrastructure spending bill, offers the potential for additional positive economic impact. The Federal Reserve, while expected to raise rates three times in 2018, continues to take a cautious, measured approach to monetary policy. Inflation is in check. Volatility is still low. Some would call this a “goldilocks” environment for investors.

2017 was an excellent year for stocks. 2018 has the potential for another strong year. However, stocks are in a bull market until they are not. To continue surviving (and thriving) in the current environment, we’ll leave you with two of our favorite investing quotes:

“If you have trouble imagining a 20% loss in the stock market, you shouldn’t be in stocks.” – John Bogle

“There will always be bull markets followed by bear markets followed by bull markets.” – Sir John Templeton

Risk is part of the financial markets, as are longer-term rewards. The key to surviving a bull or bear market is finding the right balance between risk and reward for your particular situation – our primary goal at The ETF Store.

Lastly, we wanted to share a unique and stunning image recently captured by a long-time, valued client. The photo depicts an early morning “crescent moon rising” over the Kansas City skyline. We hope you enjoy it as much as we do (it’s now hanging in our ETF Store offices)!

Courtesy of Craig McCord Photography. Scenic Impressions and the Pursuit of Light.

Courtesy of Craig McCord Photography. Scenic Impressions and the Pursuit of Light.