The following was authored by Hollie Fagan, Head of BlackRock’s Registered Investment Advisor business.

When it comes to taxes and investing, it’s all about the end game—the less you pay now, the more you’ll keep working toward your long-term goals.

As the final months of 2017 gallop to a close (wasn’t it just Memorial Day?), many of us are thinking about taxes and looking for ways to reduce the bill from Uncle Sam.

Your investment portfolio is an important part of that review. A recent BlackRock survey found that 44% of investors say taxes are the costs that matters most to them (Source: GfK, BlackRock, 8/31/2017). There’s a good reason for that: Taxes can take a big bite out of returns.

To that end, here are three tax-smart tips to think about as you prepare for year-end:

1. Seek to limit capital gains distributions

When a fund manager sells a security at a profit, the gain can come back to you as a taxable distribution, even if you don’t sell your fund shares or the fund itself posts a loss. The impact to your bottom line can be significant, as the example shows below. This year may offer some particularly unwelcome surprises, given the stock market’s strong performance.

Investments to consider: Try to reduce or even eliminate capital gain distributions in your taxable accounts. One way to try to do that is with exchange traded funds (ETFs). Because ETFs seek to track the market, they typically turn over securities less frequently than strategies seeking to beat the market; this lower turnover may result in lower capital gains; these vehicles can also be structurally tax efficient. In fact, there are ETFs that have never distributed a cap gain.

2. Be thoughtful about investment income

The other taxable distribution to look out for is the dividend. Certain fund dividends (think taxable bonds and REITs) may be subject to ordinary income tax rates. But there are several ways to possibly lighten the burden. One is location: Consider allocating your least tax-efficient investments to the most tax-friendly accounts. Another consideration is timing: If you’re planning to buy shares, pay attention to when your fund pays out dividends (known as the ex-dividend date). Because the share price may drop temporarily after payment, you could find yourself not only with a capital loss but owing taxes on the dividend.

Investment to consider: The interest from municipal bonds is generally free from federal taxes and often state taxes as well, depending on your state or where you file—savings that may potentially translate into higher returns. And dividends from stock funds (including preferred stocks) are typically considered “qualified income;” although you’ll owe taxes, they may be at the lower capital gains rate.

3. Ask for help

Taxes are complex and most of us would prefer to pay as little of them as possible. Your financial advisor or tax professional can bring crucial insight and perspective into the process. While the BlackRock survey found that 44% of investors say their advisors actively mitigate taxes in their portfolios, 37% don’t know whether they do so (Source: GfK, BlackRock, 8/31/2017). The best thing to do is…ask and learn.

Taxes are only one facet of an investment plan. Your portfolio should ultimately reflect much more: your timeframe and objectives, the risk you’re willing to bear for the performance you want and the best value for your money—including how much you pay in taxes.

Carefully consider the Funds’ investment objectives, risk factors, and charges and expenses before investing. This and other information can be found in the Funds’ prospectuses or, if available, the summary prospectuses which may be obtained by visiting www.iShares.com or www.blackrock.com. Read the prospectus carefully before investing.

Investing involves risk, including possible loss of principal.

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the date indicated and may change as subsequent conditions vary. The information and opinions contained in this post are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This post may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any of these views will come to pass. Reliance upon information in this post is at the sole discretion of the reader.

The strategies discussed are strictly for illustrative and educational purposes and are not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. There is no guarantee that any strategies discussed will be effective.

This post contains general information only and does not take into account an individual’s financial circumstances. This information should not be relied upon as a primary basis for an investment decision. Rather, an assessment should be made as to whether the information is appropriate in individual circumstances and consideration should be given to talking to a financial advisor before making an investment decision.

This material does not constitute any specific legal, tax or accounting advice. Please consult with qualified professionals for this type of advice.

Investment comparisons are for illustrative purposes only. To better understand the similarities and differences between investments, including investment objectives, risks, fees and expenses, it is important to read the products’ prospectuses. When comparing stocks or bonds and iShares Funds, it should be remembered that management fees associated with fund investments, like iShares Funds, are not borne by investors in individual stocks or bonds.

Transactions in shares of ETFs will result in brokerage commissions and will generate tax consequences. All regulated investment companies are obliged to distribute portfolio gains to shareholders.

The iShares Funds are distributed by BlackRock Investments, LLC (together with its affiliates, “BlackRock”).

The role of commodities in a portfolio is the subject of intense debate among investors. Jason Bloom, Global Market Strategist at PowerShares, offers his perspective on the value of owning commodities and highlights two broad-based commodity ETFs. Nate & Conor also preview the upcoming guest lineup on the show and explain some interesting parallels between bitcoin and ETFs.

Investment returns garner headlines, but saving money can carry far greater importance to long-term financial success. Nate & Conor detail the surprising numbers crunched by Pension Partner’s Charlie Bilello and explain how saving money is one of the few things investors can control. Also, Dave Wahl, Senior Portfolio Specialist at Rare Infrastructure, spotlights the Legg Mason Global Infrastructure ETF (INFR).

Nathan Geraci is President of The ETF Store, Inc. and host of the weekly radio show “The ETF Store Show“.

“If it’s obvious, it’s obviously wrong.” – Joe Granville

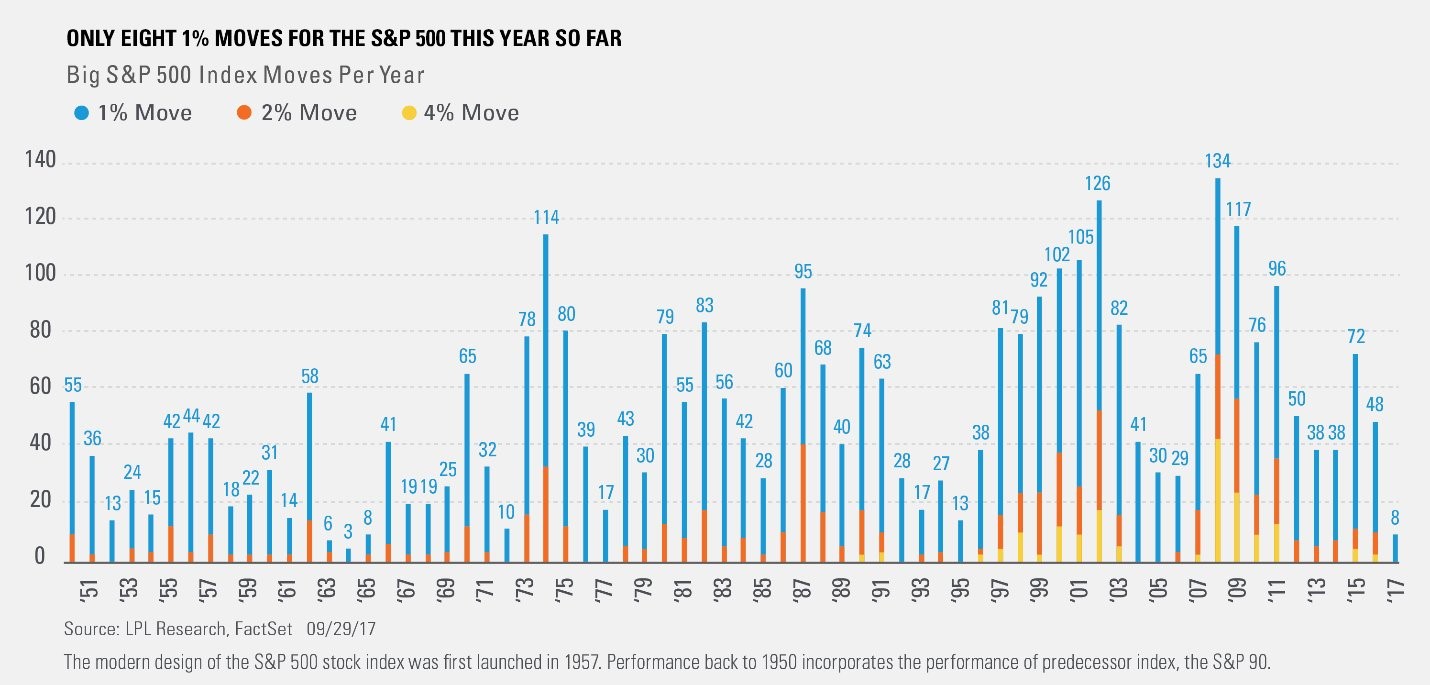

U.S. stocks set new record highs during the third quarter despite major hurricanes, political drama in Washington, nuclear threats from North Korea, and the Federal Reserve announcing the removal of stimulus. Also, a key measure of stock market fear – the volatility index or VIX – remained near record lows. As a matter of fact, 2017 is tracking as one of least volatile years in S&P 500 history.

As stocks continue their ascent, news headlines are increasingly becoming populated by a word that might send a shiver down the spine of many investors – “bubble”:

Bubbles Are ‘More Bubbly’ Than Ever, Warns BAML – September 5th, Bloomberg

Gallo Sees ‘Asset Bubbles in the Market Everywhere’ – September 11th, Bloomberg

Legendary Investor Julian Robertson Warns of Bubble Trouble – September 12th, Institutional Investor

It’s possible the stock market could be in a bubble, says ex-Wells Fargo CEO Kovacevich – September 19th, CNBC

This chart shows how the stock market is ‘smack dab at the heart of bubble territory’ – September 21st, MarketWatch

Successful investors tend to view markets with a healthy dose of skepticism. No investor wants to relive the dotcom bubble or financial crisis. The further stocks climb, it seems only natural that investors become more concerned that the “next shoe could drop” and begin to consider whether dialing back risk in their portfolios is the most prudent course of action. “Don’t get left holding the bag”, investors surmise. However, there is an interesting aspect to the current market environment that bears mentioning: historically, stock market bubbles are marked by euphoria where investors throw caution to the wind and trade stocks tips with their taxi (or now Uber) driver. Bubbles are not typically accompanied by a seemingly common opinion that we are actually in a bubble. So, what is the real consensus market opinion right now? If the stock market is surging ahead without fear, is the investor consensus predominately bullish? Or, is the market consensus the growing cacophony of investors claiming the stock market is in a bubble? The skeptical investor in us is wondering whether the “contrarians” are actually the consensus.

Investopedia defines contrarian investing as “a type of investment strategy distinguished by buying and selling against the grain of investor sentiment during a specific time.” They go on to say, “Many contrarians have the view of the market as an eternal bear market.” We might suggest this definition has actually flipped, with contrarians now viewing stocks as an endless bull market. The new consensus seems to constantly predict the market’s demise. It is within this context that we think taking a contrarian approach to investing will yield greater success. While there is obviously no such thing as an endless bull market (much to our dismay), until there is euphoria, investing against the grain and staying the course is the more sensible investment approach. But why?

“Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves.” – Peter Lynch

The dotcom bubble and financial crisis undoubtedly left deep psychological scars on large numbers of investors, causing them to invest much more conservatively than normal over the past 8+ years. According to a recent Wells Fargo/Gallup poll of U.S. investors, 26% said they still haven’t bounced back financially from the stock market downturn in 2008 – 2009. Furthermore, 54% expect a decline this year that will wipe out significant gains. This bearish sentiment has led to substantial underperformance, both from individual investors and professional money managers. As stocks continue surging ahead, market pessimism only seems to magnify with each new record high.

Claims of a stock market bubble may very well be proven “correct”, but at what price? And, are investors making these claims really “right” if they attempt to prosecute this case for years on end? Looking back at the history of the S&P 500, there have been declines of at least 19% in every decade since the 1920s – in some cases, multiple times in the same decade and with much greater than 19% losses. Sharp stock declines happen with regularity. It’s not really going out on a limb predicting a significant market pullback. Unfortunately, there are behavioral biases engrained in all of us resulting in a natural tendency to preoccupy ourselves with the monster we can’t see or don’t know. There is a reason fear sells in the financial media (which some opportunistic money managers have picked up on). Have you ever noticed that CNBC runs primetime market specials when stocks decline by 3%, but not when stocks rise by 3%? A movie, The Big Short, was made based on investors betting big against the housing market and stocks in 2007. We are still waiting for the movie on the investor who bet big on stocks in March of 2009.

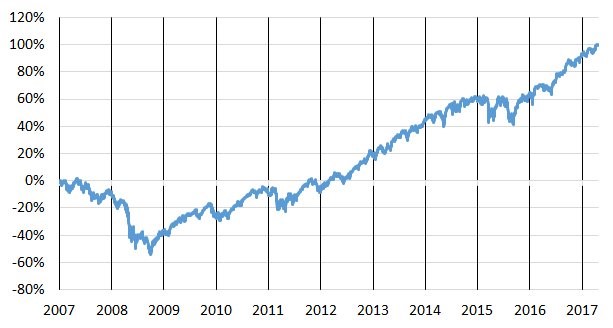

The problem with investing based on fear is the price you pay is ultimately dear. Even if you had bought stocks at the exact peak of the market in October 2007 and held throughout the financial crisis, including the full 55% drawdown through March 2009, you still would have doubled your money through the end of September! Waiting for the next shoe to drop can be a costly investment strategy.Source: @EconomPic

“Successful contrarian investing requires us to live with discomfort, for being “wrong” and alone.” – Robert Arnott

There are several important takeaways here:

If everyone is claiming there’s a market bubble, there probably isn’t one. If we were in a bubble, you likely wouldn’t know it.

Successful investing usually feels uncomfortable. Making money in any aspect of life typically requires hard work and perseverance. As they say, “if it was that easy, everyone would do it”.

Don’t let the financial media derail your investment plan. Staying current on market information can be educational, but taking meaningful portfolio action based on news flow is dangerous.

Take only the risks you are comfortable with in your portfolio. If you can’t behaviorally or financially withstand the downside of an investment, stay away from it.

Maintain the proper investment temperament. Being too bullish is never a good thing, nor is being too bearish. The Wall Street Journal’s Jason Zweig recently said, “You can’t survive a market crash if you think it can’t happen.” We would add to that: “you can survive a bull market if you think it can happen”.

Jeremy Goff, Director of Strategic Development at Tortoise, joins us in studio to explain investing in essential assets, including through the Tortoise North American Pipeline ETF (TPYP) and the Tortoise Water Fund (TBLU). Nate & Jason discuss year-to-date global stock market returns and spotlight the Global X Lithium & Battery Tech ETF (LIT).