Stocks turned more volatile during the third quarter, though still continued on their upward march. After an early August swoon, the S&P 500 reasserted itself and is now sitting near an all-time record high. The quarter was characterized by mixed economic signals and the Federal Reserve cutting interest rates for the first time since the 2020 Covid pandemic. The Fed continues searching for the delicate balance between maintaining a healthy employment backdrop and reining in inflation. Meanwhile, investors are keeping a wary eye on corporate earnings, escalating geopolitical tensions in the Middle East, the upcoming Presidential election, and the impact from catastrophic hurricanes in the southeast. Last quarter, we introduced the theme of broad crosscurrents in the markets. As the third quarter unfolded, it was clear the various crosscurrents we identified would continue driving the primary opportunities and challenges in financial markets moving forward.

Federal Reserve’s Rate Cut and Inflation

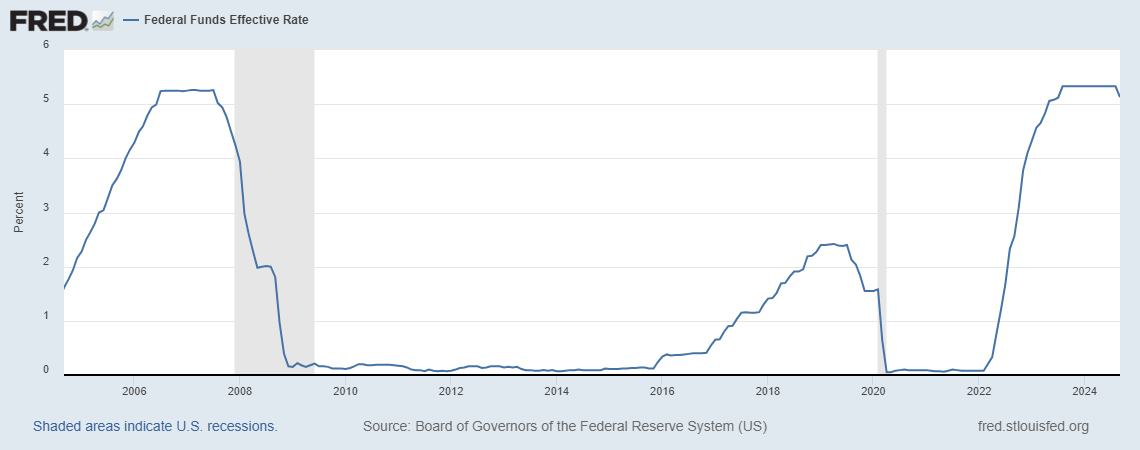

The Fed delivered a surprising 0.50% interest rate cut in September, marking its first rate decrease since March 2020. Investors had been expecting a 0.25% reduction, but the Fed clearly saw enough softening in the labor markets and progress on the inflation front to move more aggressively. Notably, outside of the Covid pandemic timeframe, the last time the Fed cut rates by this amount was during the 2008 global financial crisis.

The agency provided the following statement with the rate cut:

“The Committee has gained greater confidence that inflation is moving sustainably toward 2 percent, and judges that the risks to achieving its employment and inflation goals are roughly in balance.”

“Balance” is the key word here, specifically whether the Fed can maintain this balance. As we have discussed numerous times previously, the Fed is attempting to orchestrate what is referred to as a “soft landing”. They want to bring inflation down without causing an economic recession. Simply put, if they lower rates too aggressively, it is possible that inflation reignites. If the Fed is not aggressive enough, the labor market (and broader economy) could roll over. Thus, they need to strike the right balance. Fed Chairman Jerome Powell:

“We know that reducing policy restraint too quickly could hinder progress on inflation. At the same time, reducing restraint too slowly could unduly weaken economic activity and employment. In considering additional adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks.”

We know this is all a bit tedious, but believe the Fed’s ability to balance these risks and successfully walk the tightrope is perhaps the most critical factor impacting markets over the next several quarters. While we remain optimistic the Fed will be effective in doing so, we have also seen enough over the past several years to suggest that some caution is warranted. Remember, it was only a few short years ago that the Fed allowed inflation to ignite in the first place.

Corporate Earnings in Focus

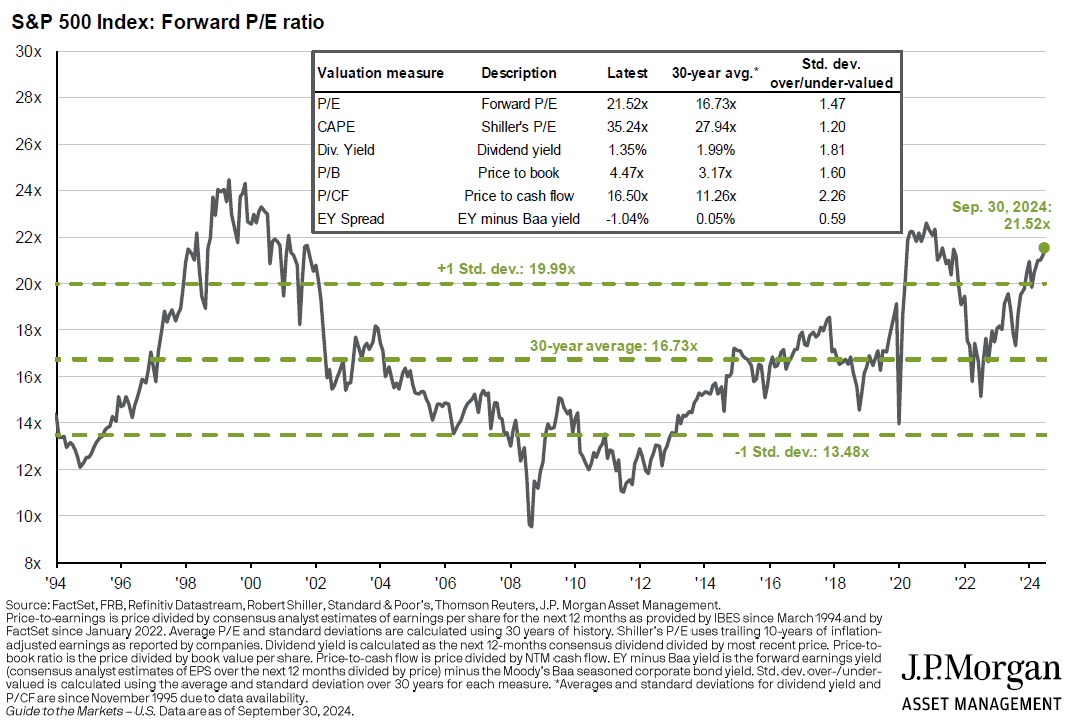

Besides the Fed’s balancing act, our focus remains squarely on corporate earnings – the single biggest factor driving longer-term stock returns. Last quarter, corporate earnings reflected a mixed picture with some consumer-focused sectors showing resilience, while others faced challenges amid changing spending patterns. Consumer spending typically accounts for about 70% of GDP in the U.S., making it a clear driver of corporate earnings. While consumer sentiment has stayed relatively strong, ongoing inflationary pressures coupled with elevated energy costs have led to more cautious spending this year. This obviously ties back into the Fed’s balancing act. If the Fed can successfully orchestrate a soft landing, that should help bolster consumer spending and companies’ ability to continue producing on the bottom line. With stock valuations currently on the higher side, that will be imperative in our opinion.

Source: J.P. Morgan Guide to the Markets

Other broad factors potentially impacting markets include escalating geopolitical tensions in the Middle East, the upcoming Presidential election, and the impact from two tragic hurricanes in the country’s southeast. While all of these bear monitoring, history tells us that any market impact will likely be short-lived. We do believe it’s important to always track these types of events from a risk management perspective, but they are not typically actionable for longer-term investors. That is not to say there aren’t examples where the shorter-term impact could be more meaningful. If the events in the Middle East cause the price of oil to spike, that could theoretically result in inflation reaccelerating and place additional burden on the Fed. If we experience another contested Presidential election, that would no doubt cause some anxiety within the markets. Catastrophic hurricanes can have some economic impact and put pressure on areas such as insurance prices and the cost of building materials. However, these types of events and their shorter-term impact will always come and go. Over the longer-term, the trajectory of the stock market remains positive.

Staying the Course

Looking ahead to the remainder of the fourth quarter, our expectation is for the mixture of resilience and volatility across financial markets to continue. The economy remains strong overall, but shorter-term crosscurrents could cause some unpredictability. As always, we will keep you informed regarding any market developments during the quarter, while staying the course on our longer-term plan to help you achieve your financial goals.

Thank you for your continued trust in our team of advisors!