The first quarter of 2024 continued the positive momentum from last year, with global financial markets navigating through a complex landscape of opportunities and challenges. US stocks, in particular, saw robust performance, buoyed by investor optimism over a resilient economy. Despite sticky inflation, ongoing geopolitical tensions, and some apprehension over the upcoming election cycle, the S&P 500 managed to maintain its upward trajectory, further solidifying the gains of the previous year.

Opportunities, optimism, and resilience are themes we highlighted last quarter, noting that successful investors always let these guide the way. An investment approach built with these as the foundation has continued to serve investors well over the past three months and will do so moving forward. We also emphasized the importance of risk management and remaining adaptive. Given the current complex economic and market backdrop, we wanted to share some thoughts on that side of the ledger as well.

You may recall that in January, we said the following regarding potential challenges:

“Will the Federal Reserve effectively balance inflation control with economic growth? On the note of economic growth, what happens with employment and consumer spending? The job market is still relatively robust, but consumer spending seemingly reflects a more cautious approach. What about the geopolitical backdrop? Will global tensions continue to rise or subside? And one more important item… it is a Presidential election year.”

Let’s briefly address each of these in pieces.

The Fed’s battle against inflation remains front and center. The economy is currently at an interesting crossroads because unemployment is still low and consumer spending remains healthy overall. However, the consumer price index – a key measure of inflation – rose 3.5% in March and remains well above the Fed’s comfort level. As we all can attest, everything is more expensive – groceries, eating out, utilities, health insurance, auto loans, credit cards… the list goes on. While the economy appears in decent shape, the question is whether the average consumer can continue shouldering the burden of higher costs.

Data suggests the room for error in household personal finances is becoming slimmer. Consumer credit delinquencies are increasing and savings rates are declining. At some point, consumers may have to curtail aggressive spending trends. That is highly important, because consumer spending plays a vital role in corporate earnings. From a longer-term perspective, earnings are the single biggest factor in the direction of the stock market. With current stock valuations on the higher end, companies will need to continue producing on the earnings side. While there is reason to believe companies can do so, the health of the consumer is paramount and the Fed’s role in battling inflation will be a critical piece to this puzzle.

As it pertains to rising geopolitical tensions, history shows that their longer-term impact is mostly inconsequential. Geopolitical events typically only impact markets on a shorter-term basis, and not always in predictable ways. That said, the ongoing Russia-Ukraine war and rising tensions in the Middle East are helping drive-up commodity prices, which can further inflame inflationary pressures. For example, there has been a recent uptick in the price of oil. With summer driving season on the horizon, the last thing price-weary consumers want to experience is sticker shock at the gas pump. This is yet another variable the Fed will have to contend with as they attempt to further rein in inflation.

There is admittedly a lot to digest here, but this interplay between the Fed, consumers, corporate earnings, and geopolitics will likely dictate the future direction of markets overall. As mentioned previously, while we always remain optimistic over the longer-term, we are vigilantly monitoring these relationships in the shorter-term.

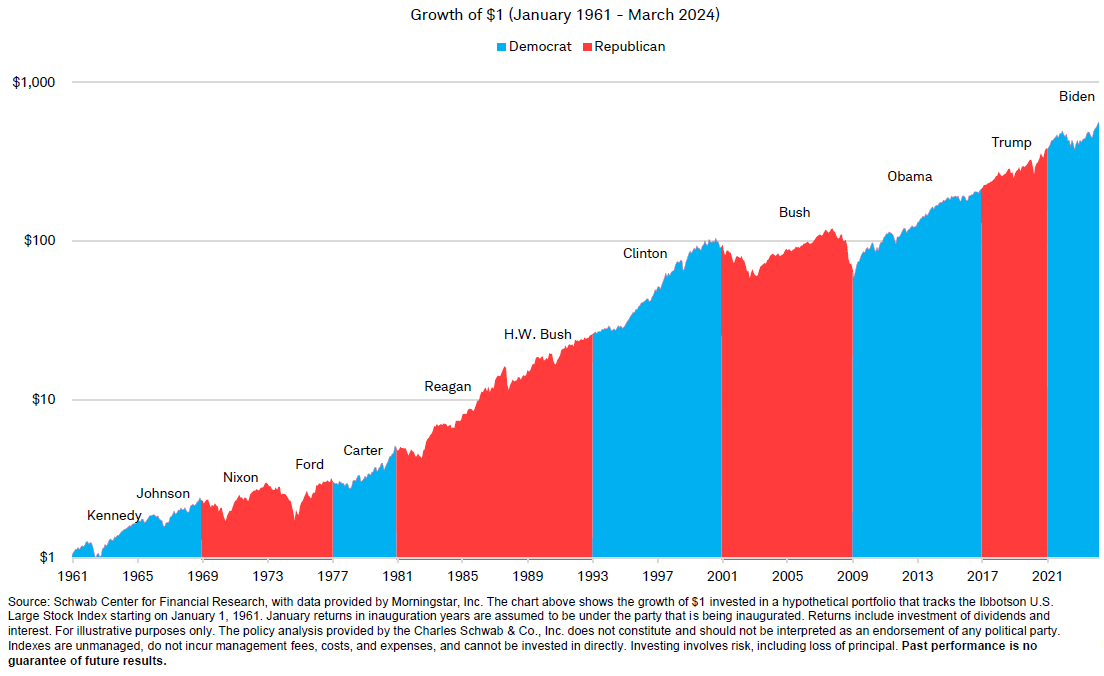

Finally, a brief note about November’s upcoming election, which can cause anxiety for some investors. In general, people tend to feel better about the stock market and economy when their political party of choice is in power. But if you look at the data, there is not really a discernable pattern in terms of whether we have a Republican president or Democratic president, who controls Congress, or unexpected shifts in policy. Longer-term, the direction of stocks is up.

Source: Charles Schwab

Our message is always the same when it comes to elections: “Don’t mix politics with portfolios”. That is not to say the election and hoopla around it can’t cause some shorter-term volatility or even a meaningful decline. The challenge is that it’s not typically predictable or investable in any way.

As we look ahead to the remainder of the year, opportunities and challenges will continue to present themselves. Our commitment to you remains the same. We will stay informed on both, while prioritizing important items we can control – namely global portfolio diversification, maintaining discipline, and keeping a longer-term perspective. As always, we appreciate the trust you have placed in us to help navigate your financial journey and our team of financial advisors is here to answer any questions you may have.